Introduction: India as a High-Potential Business Destination

India is quickly becoming a key player on the world stage for entrepreneurs. Its economy is on course to reach $5 trillion by 2027, driven by advances in technology, a booming startup culture, and one of the youngest workforces anywhere. There are more than 2.8 million registered companies in India, with over 159,000 of them officially listed as startups.

These numbers reflect a country buzzing with business energy. From Fortune 500 giants to emerging disruptors, enterprises are building GCCs, R&D hubs, and shared service centers here—not just to save costs, but to unlock scale, innovation, and agility. But offshoring to India requires more than optimism—it demands structure, regulatory navigation, and strategic intent.

Here’s your offshore-readiness roadmap:

1. Choose the Right Business Structure

The business structure you pick has long-lasting effects—it influences your taxes, your responsibilities, and even how easy it is to raise money. Choosing wisely at the start can save headaches down the line.

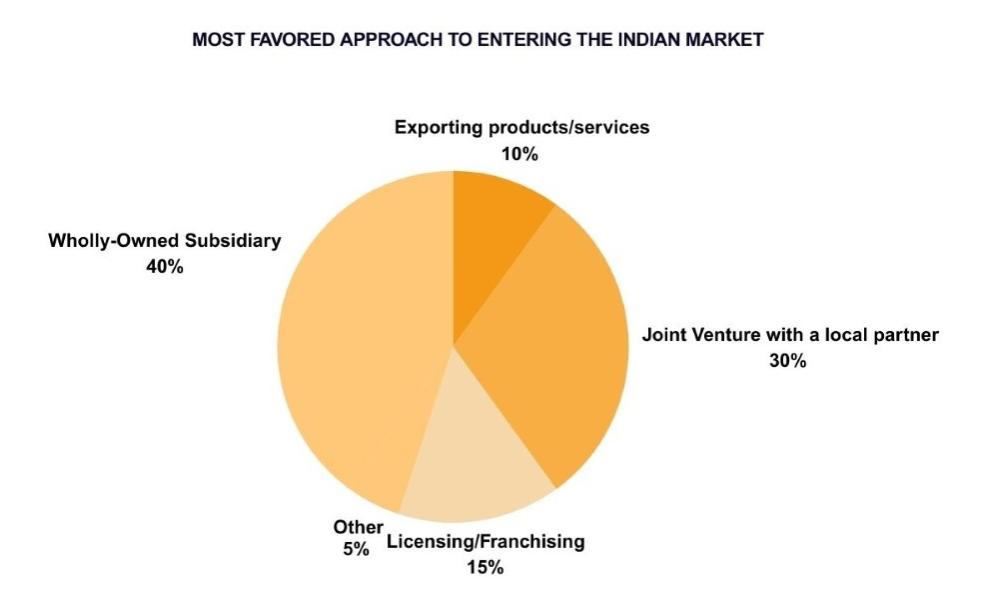

Most favoured approach to entering the Indian market:

- Private Limited Company (PLC): This is the go-to for startups that want to grow fast and bring in investors. It protects your personal assets and is trusted by banks and investors alike. According to SRKay’s research, 42% of C-suite leaders prefer a Wholly-Owned Subsidiary structure to retain full control.

- Limited Liability Partnership (LLP): LLPs work well for smaller companies, especially service providers. They blend the flexibility of partnerships with some liability protection, and the paperwork isn’t as heavy.

- One Person Company (OPC): If you’re flying solo, OPC offers the perks of limited liability but with simpler management.

- Public Limited Company: For big businesses looking to raise capital publicly, this structure is necessary but comes with stricter rules.

- Partnership: Easy to form and popular for small teams, but remember, partners have unlimited liability, which can be risky as the business grows.

The key is to match the structure to your long-term goals, not just what’s easiest in the moment.

2. Secure a Digital Signature and Director Identification Number

Before you can register your company, every director needs two things:

- Digital Signature Certificate (DSC): This lets you sign documents electronically—no need for printing and scanning.

- Director Identification Number (DIN): A unique number given by the government to every director, so they can be tracked in official records.

These require documents like your PAN card, Aadhaar, and proof of address. The process usually takes just a few days if your paperwork is in order.

3. Reserve Your Business Name

Your company’s name is your brand’s foundation. You apply for up to two names through the government’s SPICe+ portal. The names need to be unique, meet naming rules, and not clash with trademarks. This step isn’t just bureaucratic—it’s about protecting your brand from legal troubles later.

4. File Your Incorporation Documents

After your name is approved, you fill out Part B of the SPICe+ form. You’ll need to provide:

- Your company’s registered office address

- Details of shareholders and directors

- The Memorandum of Association (MOA) and Articles of Association (AOA), which explain what your company does and how it’s governed

- Applications for PAN and TAN for tax purposes

Stamp duties apply and differ by state. The whole process usually takes a week or two, depending on how quickly the government processes your paperwork.

5. Obtain the Certificate of Incorporation

When your documents clear all checks, you get your Certificate of Incorporation plus your PAN and TAN numbers. This means your company officially exists, can open bank accounts, and legally operate.

6. Register for Licenses and Statutory Taxes

Forming the company is only the start. Depending on what you do and where, you might need various licenses:

- GST Registration: Mandatory if your turnover goes beyond a certain point. GST simplifies indirect taxes across India.

- MSME Registration: If your business qualifies, registering here unlocks access to government support schemes.

- Trade License: Local authorities issue these to regulate business operations and safety.

- Specialized Licenses: Food businesses need FSSAI permits, import-export firms require an IEC code, and shops need Shops and Establishments licenses.

Some states, like Telangana and Tamil Nadu, offer faster approvals through single-window clearances, which cuts through a lot of red tape.

7. Manage Post-Registration Compliance

Compliance is ongoing:

- Open a corporate bank account under your company’s name.

- Register your employees for EPF and ESI if applicable.

- Keep detailed records of shareholders, directors, resolutions, and meetings.

- File annual financial statements and returns with the Ministry of Corporate Affairs on time.

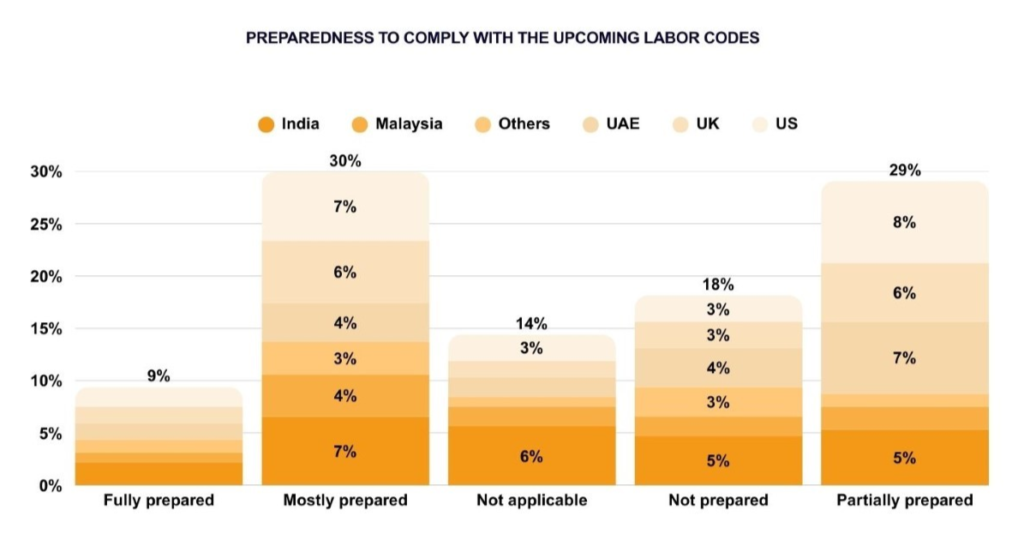

Many companies struggle here—recent research shows only 9% feel ready for full compliance, so staying on top of this is critical.

Beyond Registration: Strategic Market Entry Planning

This is where India strategy becomes a business function.

- Decide whether your focus is selling directly to Indian customers or using India as a base for operations.

- Understand that regulations and incentives vary widely between states.

- Do your homework on compliance, partnerships, and environmental or social governance factors.

- Pick your location carefully, balancing cost, talent pool, and infrastructure. For instance, Gujarat and Tamil Nadu offer capital subsidies up to 25% for eligible sectors.

- Consider sector-specific challenges—pharma, tech, retail—they each have their own quirks.

- Build strong governance and compliance practices from the outset; this pays off as you grow.

To explore each of these pillars in depth, download the full SRKay whitepaper—your practical guide for navigating India’s evolving business environment.

Conclusion: Turning Plans into Progress

India offers huge opportunities, but success demands more than just following rules. It requires clear planning, focus, and a deep understanding of the market. Businesses that prepare well and stay disciplined will not only launch effectively—they will lead.